It has long been agreed that the primary responsibility of a Central Bank is to control inflation; therefore, every central banker evaluates their performance based on the level of price stability achieved during their tenure. For Olayemi Cardoso, this was no exception. Since his inception as the Central Bank Governor of Nigeria he has made a concerted effort to rescue the battered Nigerian currency, which had become one of the worst-performing currencies globally, and alleviate the resulting inflation, which had reached unprecedented levels since the return of democracy to the country.

Olayemi Cardoso graduated from the University of Aston in Birmingham, United Kingdom, in 1980 with a Bachelor of Science in Managerial and Administrative Studies with concentration in Finance and Accounting and subsequently pursued his master’s in public administration and Management, again with concentration in Economics and Finance from Harvard University. Olayemi Cardoso has had a remarkable career in the banking sector, spanning approximately 29 years culminating in Olayemi Cardoso becoming the Chairman of Citibank Nigeria Ltd, a subsidiary of the world’s leading global bank and the oldest international bank in Nigeria, from 2010 to 2022. Cardoso also served as Commissioner for Economic Planning and Budget, Lagos State Government, from 1999 to 2005. Olayemi Cardoso is also a Fellow of the Chartered Institute of Stockbrokers.

For the past six months, Olayemi Cardoso led Central Bank of Nigeria (CBN) has been engaged in a protracted battle to salvage the Nigerian currency, curb inflation, and restore stability to the market. Markets become dysfunctional when prices are unstable, and businesses cannot plan when prices are not stable. The CBN had announced in June 2023, two months before the appointment of Olayemi Cardoso the floating of the naira in the Importer and Exporter window, now called the NAFEM market on FMDQ by removing the purchasing and selling caps thereby allowing a willing seller and buyer to determine the price of the naira. This move caused the naira’s value to move from N400 in the official market to N700 per dollar.

The thinking behind the floating of the naira which Olayemi Cardoso on appointment has sustained was that it was necessary to eliminate arbitrage, which had created overnight billionaires, and achieve FX unification that will trigger greater FX inflow a long-sought goal by investors which President Tinubu had promised during his campaign

Olayemi Cardoso and the Value of Money

Where does a currency derive its value from? In the past century when the Gold standard was the norm, paper currency in circulation was pegged to the value of gold held by the central bank of that country. Assuming a country has 10 trillion worth of paper currency in circulation, the amount of gold held by the central bank should correspond to 10 trillion. Consequently, the value of any paper currency must correspond to a percentage value of gold.

Economists of that time viewed this as a significant limitation to economic prosperity, as it constrained the government’s ability to intervene using monetary tools. John Maynard Keynes, the founder of the Keynesian model, was a vocal critic of this model, advocating for increased government intervention to stabilise the market and end the continuous cycle of boom and bust within the European economies.

World War II brought the European and global economies to ruins with excessive debts owed to the USA, hence the move to end the gold standard began. In 1944, at the international conference held at Bretton Woods in New Hampshire, United States, and attended by representatives from 44 countries, it was agreed that the US dollar would become the global reserve currency, replacing gold. However, the US dollar was still pegged to gold until 1971, when it was suspended, and fiat currency was introduced.

Fiat currencies are created by governments and, unlike the gold standard, where paper currency has to correspond to the value of gold in reserves, fiat currencies are backed by nothing beyond the trust of the government and the rate of its global demand. Governments are free to print money as needed to spend to reflate its economy when necessary. As seen in Zimbabwe, Venezuela, Argentina, and others, excessive creation of fiat money destroys the value of a currency and triggers an FX run, depriving the country of much-needed FX for imports.

A View of the Naira Crisis

There are multiple ways to comprehend the Nigerian FX crisis. Firstly, it is essential to understand that since 1944, when the Bretton Woods agreement was reached, with the US dollar becoming the global reserve currency, every country keeps dollars as a reserve in place of gold, though some still keep both-countries are presently diversifying their reserves away from the dollars. FX reserves are used to fund imports, pay off foreign debts, and intervene in the market when dysfunctional. FX reserves are earned through the basic law of demand and supply. When an economy exports a product to another, it earns dollars. When it imports products from other countries, it exchanges the naira it has with the dollar to fund import. There are other means to earn FX, such as remittances

When your uncle in the UK or anywhere across the globe sends you money to pay for your school fees or to assist him to build a house, it amounts to a remittance. Any money sent directly by diasporas to their country to beneficiaries is called remittance. Other methods of earning FX include foreign borrowings, Foreign Direct Investments (FDI), grants and aids and Foreign Portfolio Investors (FPI), also known as hot money due to the fast rate at which they move out at the sight of any crisis.

When a country earns dollars through any of these means, the Central Bank receives the money in its reserves and converts the equivalent to its local currency. Similarly, when a country seeks to import, the local currency is exchanged with the dollar. However, with the float of the naira sellers and buyers can take their money directly to an FX market, in this case, the NAFEM Market and trade. FX can also be traded in the parallel market and with the rise of cryptocurrencies it can also be traded in crypto exchanges where USDT is pegged to the USD.

Theoretically, the value of a currency comes from the interactions between the demand and supply of the local currency and the dollar, the global reserve currency. However, this is not the whole story. Nigeria has a surplus Current Account balance and a healthy trade balance. According to the Nigerian Bureau of Statistics (NBS), the total volume of trade in Nigeria in 2023 was N71.8 billion, of which imports were N35.917b while export was N35,962 leaving a Current account of about N45m.

So, why is the Nigerian currency still weak to the dollar when the trade statistics show a ratio of 1:1 in demand and supply?I will be the first to say that the foreign trade statistics doesn’t capture invincible demands for the dollar such as for school fees, BTA, medicals, subscription services and other invincible demands which amount to billions of dollars annually.

Secondly, because Naira is a fiat currency, the Nigerian government regularly uses ways and means to regularly inject naira liquidity to the economy especially as its revenue keeps diminishing in the wake of troubles in its oil sector while government expenditure keeps expanding. Liquidity within every economy is meant to match the level of productivity within that economy. When Liquidity is artificially created without a corresponding productivity it creates a distortion in the market and triggers an FX run. Cheap money encourages speculation and asset bubbles.

Over the years the Nigerian government has been using ways and means to supplement its revenue, this has quietly created a distortion in the FX market as the naira sought more dollars than it has earned creating an imbalance between both currencies. As the imbalance widened, rather than encourage more productivity or allow the laws of demand to determine the price of the NGN-USD, the government sought to hide this imbalance by continually pegging the naira to the dollar at an arbitrarily rate by using its enormous reserves earned from oil export to intervene in the market. The Nigerian government considers subsidising the rate of the naira to the USD to an FX insatiable citizens as a national necessity.

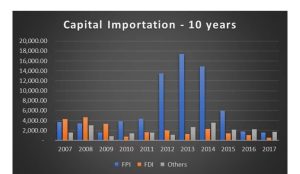

This continued till 2014 when the global oil prices collapsed after a three year high. Prior to this, Nigeria saw FDI move from circa $4b in 2007 to less than $2b in 2014. As FDI fell, FPI rose. As crude oil prices fell, FPI showed why it is called hot money and took to its heels leaving Nigeria bare. FX supply fizzled while demand remained unchanged. For political reasons, Nigeria with its depleting reserves that has lost 50% of its value since 2007 choose to still peg its currency.

The result was a wide disparity in the official market and the parallel market which grew tremendously to service the dollar appetites that the official market can no longer service. The dollar moved from a rate of circa N160 in the official market in 2014 to N197 in 2015 and to over N232in the parallel market, creating room for arbitrage and a huge decline in trust for the naira . This disparity between the official market and parallel market rates kept widening in the eight years of the Buhari government.

Fiat currency draws their value from the amount of trust placed on it by the government and by the users. As the Naira rate kept fluctuating leading to spike in inflation, Nigerians lost trust in the naira and sought to hedge their currency risk by converting naira to dollars and other FX assets. Hence, rather than become a currency for transaction, the dollar became an asset Nigerians kept due to its increasing value relative to the naira leading to hoarding and speculation of the dollar, which offered incredibly high returns.

To further make matters worse, The Buhari government pumped 27trn in ways and means into the Nigerian economy and most of the funds ended up in the wrong hands and became a tool for speculation- chasing limited dollars, hence creating a distortion in the market by further increasing the dollar rate as more people sought to purchase dollar as an asset to hedge against inflation.

this further eroded the confidence in the naira. Because naira-USD was now an asset, it was speculated on just as any other asset was leading to more volatility and resultant inflation and price instability.

Olayemi Cardoso’s Response to the Naira Crisis

Olayemi Cardoso has not kept anyone in doubt of his desire to restore confidence in the naira and achieve market stability. At his speech with the senate committee on finance he emphatically stated that the CBN will be moving away from development financing and focus on its core mandate which is price stability. To achieve this he has unveiled a number of policies to achieve his objectives

- FX Unification and the End of Arbitrage

On assuming office in September 2023, Cardoso, nicknamed the “headmaster” for his meticulous financial management skills, understood that he needed to ensure price stability quickly. In the Nigerian context, FX stability is the largest contributor to price stability, unlike in the West, where interest rates set the pace. The Nigerian economy is intrinsically tied to the dollar because Nigeria is largely a consumption economy with local productivity at near zero. To ensure price stability, Cardoso knew he needed to stabilise the naira-USD, eradicate multiple exchange rates so that investors and businesses can plan, and to remove arbitrage so that funds can be used to create real economic values.

Some have argued that the floating of the currency was misplaced and accuse the policy of being the chief reason why the naira has continued to tumble, triggering hyperinflation. I disagree with this opinion. For the eight years of the Buhari administration, I have always rejected the idea that floating would be a panacea for Nigeria’s currency crisis, which I saw primarily as a supply issue. If FX supply doesn’t improve, then floating or pegging will lead to no significant solution.

However, I understood why the currency needed to be floated by Olayemi Cardoso. With unpaid backlogs and FX forwards amounting to one-third of Nigeria’s FX reserves, it was necessary to clear them so as to induce market confidence to trigger more investments into the economy. No investor would come into Nigeria when FX backlogs are not being cleared and FX forward contracts are not honoured. Olayemi Cardoso has gone on to clear the backlogs inviting further confidence in the naira. This policy appears to be yielding results. Presently, the parallel market rate is below the official rate, which I see as an extraordinary achievement, outpacing the initial goal of unification. The NAFEM market in Q1 of 2024 is also witnessing a high FX inflow

2. War on Speculation

Olayemi Cardoso’s greatest war for price stability would be fought with speculators. Speculators are part of every market ecosystem; however, the amount of distortion they should be able able to bring to a market should be limited.

Upon floating the currency, Olayemi Cardoso-led CBN had suggested the true rate of the naira to be around N700. However, the naira has risen to a high of N1800 in February before rebounding to within N1200. The thinking is that there are too many distortions in the market that are stopping true price discovery. These distortions come from speculators who are liquid enough to make large dollar purchases as an asset to move the rate.

Olayemi Cardoso and his team had no option but to go bullish using monetary tools. The Cash Reserve Ratio (CRR) for banks was raised to 45%, the MPR rate went to 24.75%. The thinking behind this was to limit the amount of naira available to speculators to purchase dollars and also to present another investment opportunity to those who are liquid in naira. Olayemi Cardoso-led CBN has also limited the net open position of banks to 30%, hence limiting the abilities of banks to speculate and to ensure that they regularly supply FX to the market. Also, the National Security Adviser has taken on Binance, the crypto trading platform which has been accused of distorting and misleading the market.

These moves were responsible for the appreciation of the naira in March-April, with the parallel market falling below N1000. This war is not yet won, as the uncoordinated nature of the Nigerian market makes easily prone to distortions, especially the parallel market which takes care of the FX needs of thousands of MSMEs and family in Nigeria and whose signal also dictates trading pattern on the NAFEM market.

3. Increasing FX Earnings

Source-Nairametrics

There’s no confusion that the major reason for price instability in Nigeria is a direct cause of declining FX revenue, which has raised the rates of the naira to the USD. Olayemi Cardoso knows this too, and this is why he is bullish on FX stability. The hike in MPR rates has begun to attract the much-needed FX into the economy. Though FPI comes with its own risk, it is a great tool to chase cross-border capital and temporarily bridge FX gaps within the economy.

Lamido Sanusi, as the CBN Governor from 2009-2014, used this tool to great effect in stabilising FX rates. I am glad that Olayemi Cardoso has gone to this playbook to create a temporary reprieve for the badly battered naira. Reforms within the IMTOs whereby caps were removed, allowing the IMTOs to determine their quotes and spread for the dollar, are also now yielding results, as remittances have begun to improve.

4. End of Way and Means

Though Olayemi Cardoso has openly spoken of ending ways and means which are chiefly responsible for distorting the market, it appears the CBN is back to lending to the Government as a recent article by Nairametrics show.

Will this war on stability be won?

The Efficient market theory encapsulates that the price of an asset is also a function of the available information about that asset. As earlier stated, the Naira-USD is now treated as an asset and information around an asset will set its price. The naira has lost the trust of its users and aided by scaremongering on the social media and clickbait searching News media, Nigerians continue to hoard and speculate on the dollars. However, I am optimistic that the naira will rebound this year as the FG and the CBN continue a number of initiatives to improve confidence in the naira. This measure includes various diaspora bonds and a plan to issue domestic dollar bonds. Another major determinant to the fate of the naira would be the directions of the FEDS who have kept tightening rates since 2022 to curtail inflation as a result of the expansionary spending in the wake of Covid-19. The increase in interest rate by the FEDS has slowed the cross border movement of funds to emerging economies and has strengthened the dollar against all major currencies and there is no sign that the FEDS will reduce interest rates this year.

Personally, I feel that the noise on the naira rate across all media in Nigeria play a bigger role to price instability in the country. A floating currency ought to move as the rate is not pegged, perhaps due to the low level of knowledge about this, Nigerians make all manner of noise around it, triggering panic driven actions that exacerbate price movements and emboldening others to speculate and hold on to the dollar as an asset rather than a currency for transaction.

I must also say that the dollar is now the currency of corruption in Nigeria due to it corresponding value to the naira, and being a corrupt filled country, this puts enormous pressure on the dollar demand.

However, the long term aim for price stability lies on the Nigerian fiscal authorities who must do better and compliment the CBN efforts to improve the abilities of the country to earn debt free FX and also to curtail expenditure and limit its deficits.